4 March 2024, Europe, Germany | Investment Management | News

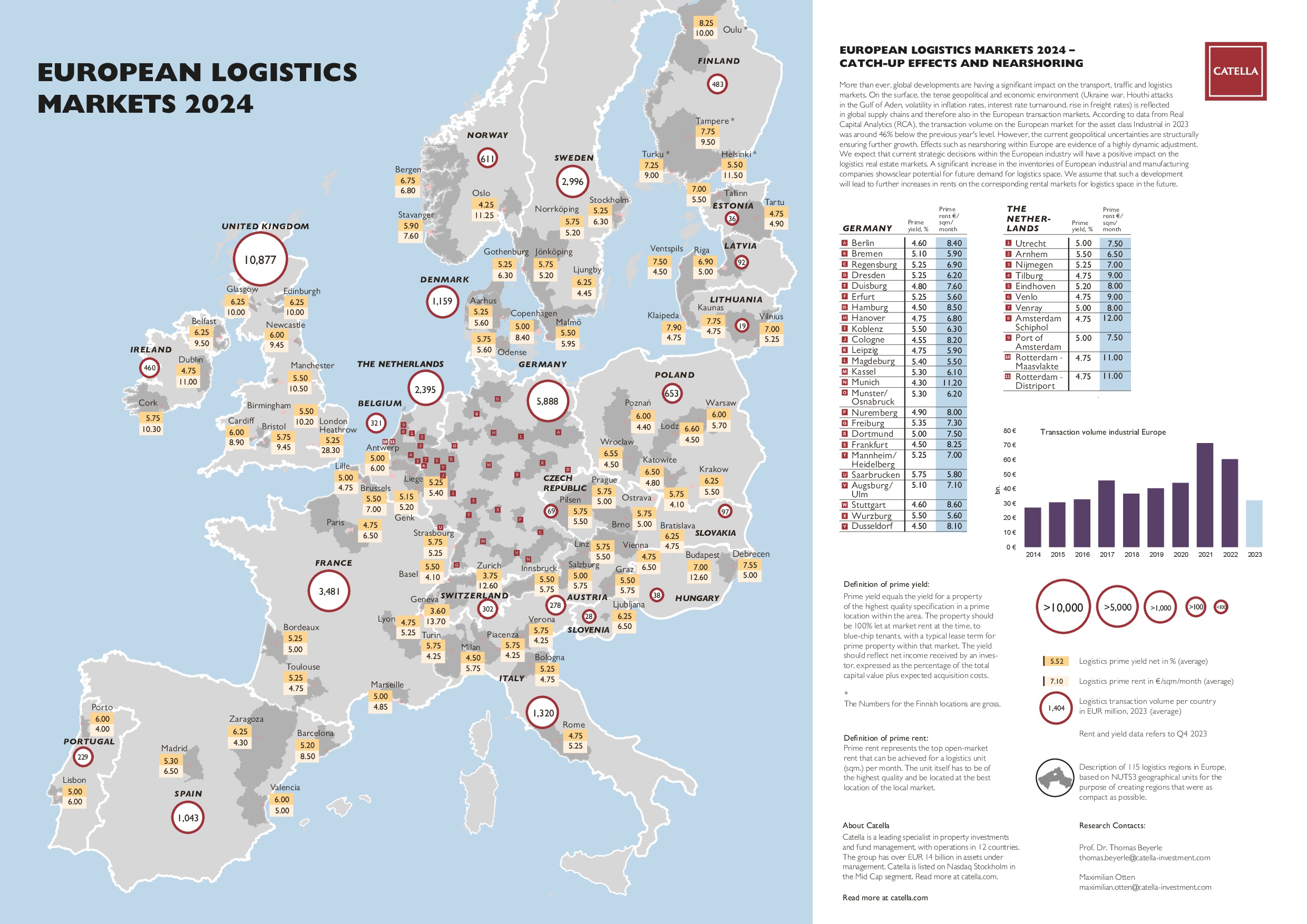

More than ever, global developments are having a significant impact on the transportation, transport and logistics markets. On the surface, the tense geopolitical and economic environment, such asthe war in Ukraine, Houthi attacks in the Gulf of Aden, volatility in inflation rates, interest rate turnaround, and rise in freight rates is reflected in global supply chains and therefore also in the European transaction markets. According to data from Real Capital Analytics (RCA), the transaction volume on the European market for the industrial asset class in 2023 was around 46% below the previous year's level.

In this environment, the logistics asset class, which has been spoiled by success in recent years, also felt the effects of repricing last year. In a nutshell, this means that yields have risen again, as have the majority of rents. Does that fit together? Definitely yes, especially as investor and tenant demand for (new-build) space with high energy requirements in preferred locations in Europe remains very high. The first effects of "nearshoring" or "relocating" in Europe can also be measured.

There have been changes in yields and rents over the last 12 months. We would like to give you an up-to-date overview of the 1st quarter of 2024 and our expectations for the logistics markets in Europe - as always in a comparative overview with a total of 115 regions:

- European prime rents currently average around €7.1/m² and range from €4/m² in Porto to €28.3/m² in London (Heathrow). Since our last market overview in March 2023, prime rents for logistics properties have risen by an average of around 21% across all 115 markets surveyed.

- The increase was particularly significant in Venlo (+73%), Edinburgh and Glasgow (around 64% each), Rotterdam (+69%) and Venray (+60%).

- Due to the new risk assessment on the European commercial real estate markets, the yield compression of recent years has come to an end. The European prime yield currently averages 5.52%, which is 66 basis points higher than in the Q1 2023 analysis.

- The top German locations have a low yield level in an international comparison (4.30% - 4.60%). The lowest yields can be found in Switzerland (Zurich: 3.75% and Geneva: 3.6%). No location in Europe fell below the 3.5 % mark.

- The continued strong demand for logistics properties is reflected in the transaction volumes for 2023. For example, the transaction volume in Germany amounted to around €5.9 billion last year. In the United Kingdom, the volume amounted to around €11 billion.

- Overall, an investment volume of almost 29 billion euros was recorded across the markets surveyed in 2023.

The European logistics market remains in a healthy state. On the one hand, the market for logistics real estate will show clear push factors for a focus on the traditional European logistics clusters in the coming months with reshoring, nearshoring and the effects of the wars in Ukraine and the Gulf of Aden. We therefore assume that the current strategic decisions of the European industry will have a positive impact on the logistics real estate markets. A significant increase in the inventories of European industrial and manufacturing companies shows clear potential for future demand for logistics space. We therefore expect such a development to lead to further increases in rents on the corresponding rental markets for logistics space in the future. We are also observing growing investor interest in Eastern European markets/properties.

DOWNLOAD CATELLA LOGISTICS MAP