2023-07-11 7:43 CET, Europe, Germany | Press release

Soaring financing rates, elevated construction costs and an onslaught of environmental legislation herald a profound realignment of European residential investment valuations as a ‘decarbonisation tipping point’ approaches, Catella’s European Residential Vision 2023 research White Paper The Epsilon - Great Transformation of Real Estate Markets concludes.

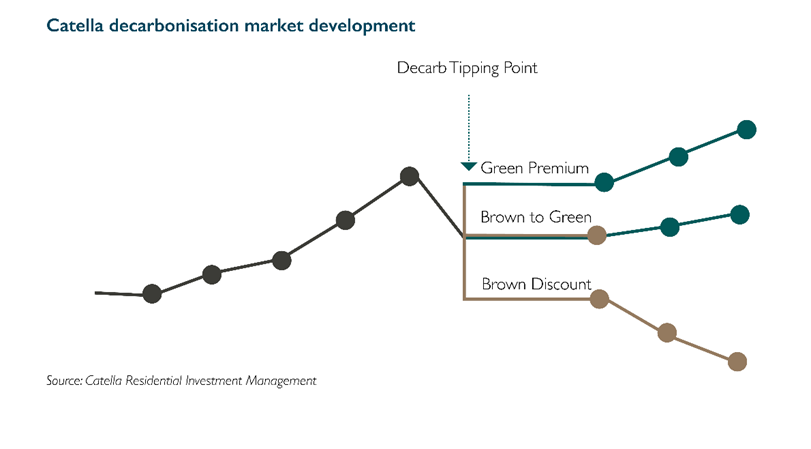

Xavier Jongen, Managing Director, Catella Residential Investment Management, said: “We believe the real estate realignment is underway as markets start to understand that the valuation gap will continue to widen between assets with a ‘brown discount,’ which are not sustainable in their current composition, and those with ‘green premiums,’ or the highest decarbonisation and increasingly societal well-being credentials. In this new paradigm, the European residential transaction market will not revert to a cyclical form, but become more a transformational ‘curve,’ dividing into a Greek letter Epsilon shape [E/ε].“

The economic productivity of the past 200 years, based on a high Energy Return on Investment (EROI) from excavating cheap and efficient fossil fuels, will decline because we are not making the necessary investments in renewables, Jongen added. GDP growth, one of the main drivers of property markets, will contract accordingly, as the economy will need to be embedded back into ecology.

For European residential markets, the journey to this ‘Great Transformation’ starts, with the recent period of ultra-loose monetary policy having pushed both square metre valuations and, as a knock-on effect, free market rents to record highs. Housing affordability and the rise in household numbers struggling to get by on their monthly incomes is at the top of the agenda for politicians and the residential industry itself across Europe.

Decarbonising existing European housing assets, an asset class bigger by value than total equities, fixed income and other financial markets combined, is a huge new business opportunity for energy consultants and construction companies, estimated at between €25,000 - €40,000 per dwelling. Decarbonising from an investment management perspective, when coupled to value creation, means taking development, redevelopment, repurposing and densification risks. This presents great opportunities, since the downside risk is limited due to strong housing market fundamentals.

Jongen concluded: “The trap will be that we do not see the Great Transformation as we analyse the piling up of crises through the lens of the known cyclical nature of the previous world order and wait to circle back in mean reversion. Long-term winners in this ‘Epsilon forking’ of the brown and green climate, and ultimately societal, pathways will be those investors and companies able to capture the emerging green premium, which also doesn’t have a generally accepted valuation tag – at least not yet.”

Read more information about the Catella White Paper here

About Catella Residential Investment Management GmbH (CRIM)

Catella launched its first European residential fund in 2007 and its first dedicated European Student Housing Fund in 2013. CRIM is a subsidiary of the Stockholm-based Catella Group, and its residential real estate business comprises portfolio management, acquisitions, sales and asset management. CRIM manages and advises several funds and mandates, and has assets under management of around €7.5 billion across 10 European countries.

For more information, please contact:

Catella Residential Investment Management GmbH

Stine Zöchling

Head of Marketing and PR European Residential

Telephone: +49 (0)30 887 285 29 76

Mobile: +49 (0)151 544 51 005

stine.zoechling[ at ]catella-residential.com