2025-05-27 7:02 CET, Europe, Germany | Investment Management | Press release

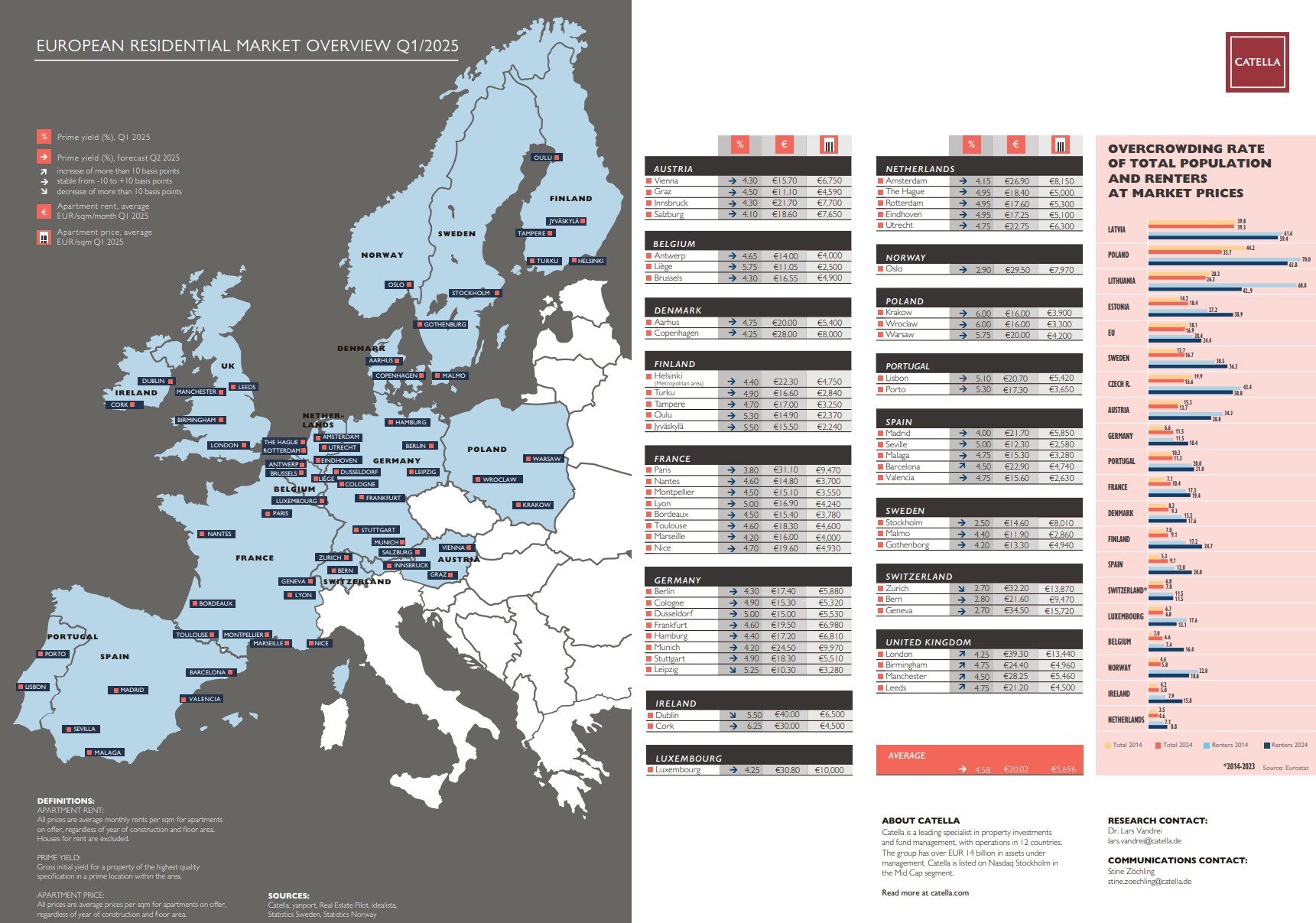

In the first quarter of 2025, rental prices in Europe continued to rise, while developments in purchase prices varied: some markets are experiencing a moderate recovery, while others are still seeing slight price declines. Persistently low levels of new construction amid high housing demand are leading to supply shortages in many cities, resulting in an increase in the overcrowding of rental apartments. These trends are analysed in the current Catella Residential Market Overview Q1/2025, which examines developments in 59 cities across 16 European countries.

Dr. Lars Vandrei, Head of Research at Catella Investment Management (CIM), comments: “The first quarter of 2025 was once again marked by considerable uncertainty. Nevertheless, we observed moderate growth in purchase prices and stabilized yields. Demand in the rental market remains strong, as reflected in rising rental prices and increasing overcrowding.”

Rental market

- Rental prices increased in 48 out of the 59 cities analysed. The unweighted European average currently stands at €20.02/m² per month, representing a 2.4% increase compared to the average of the same cities in Q3 2024.

- The highest rents were recorded in Dublin, averaging €40.00/m² (+€5.00) – also the largest rental price increase. London follows at €39.30/m² (+€1.70), with Geneva in third at €34.50/m² (-€0.20).

- The lowest rents among the cities studied were in Leipzig (€10.30/m²), Liège in Belgium (€11.05/m²), and Graz (€11.10/m²).

Property market

- Purchase prices for condominiums rose in 31 out of the 59 cities analysed. The unweighted European average price per square meter is €5,696, a 0.9% increase compared to Q3 2024.

- The highest prices were recorded in Switzerland: Geneva remains the most expensive city at €15,720/m², followed by Zurich (€13,870/m²) and London (€13,440/m²).

- The most affordable home prices were found in the Finnish cities of Jyväskylä (€2,240/m²) and Oulu (€2,370/m²).

- The highest relative price increases since Q3 2024 were seen in Copenhagen (+9.6%), Gothenburg (+10.5%), and Madrid (+11.9%).

Yields

- Average prime yields for multi-family residential properties currently stand at 4.58% (unweighted), unchanged from Q3 2024 across the same markets.

- The lowest yields were found in Stockholm (2.50%) and in Zurich and Geneva (2.70% each).

- The highest prime yields were attainable in Cork (6.25%) and in Polish cities such as Krakow and Wroclaw (6.00% each), and Warsaw (5.75%).

Focus on Germany

- Rents increased in all German cities analysed. Munich is the most expensive rental market with €24.50/m² (+€0.40), followed by Frankfurt (€19.50/m², +€0.30) and Stuttgart (€18.30/m², +€0.20).

- In the ownership market, Munich remains in the lead with €9,970/m², just below the €10,000 mark surpassed in 2022. Frankfurt (€6,980/m²) and Hamburg (€6,810/m²) follow.

- Leipzig remains the most affordable among Germany’s eight largest cities with an average price of €3,280/m² and prime yields of 5.25%.

- The lowest yields were recorded in Munich at 4.20%.

Special focus: rising overcrowding signals growing rental housing shortage in Europe

This edition includes a special focus on household overcrowding across European countries, measuring the proportion of individuals living in households that lack sufficient rooms based on their composition. In 2014, 18.1% of the EU population lived in overcrowded conditions. By 2024, this figure had slightly decreased to 16.9%. However, the share of renters living in overcrowded homes rose from 20.4% in 2014 to 24.4% in 2024 EU-wide. Overcrowding is particularly pronounced in Northern and Eastern Europe, while Western and Southern European households tend to have more living space – though notable increases are now occurring there as well: Germany (+4.9 percentage points), Belgium (+4.6 pp), and Spain (+3.8 pp), as well as Sweden (+4.0 pp), recorded significant rises in overcrowding rates in the total population. Among renters, the situation is even more acute: Belgium (+9.0 pp), Spain (+8.0 pp), and Ireland (+7.9 pp) show marked increases. In Germany, 18.4% of renters now live in overcrowded housing – up sharply from 11.5% ten years ago.

About Catella Investment Management GmbH (CIM)

Catella Investment Management GmbH (CIM) is an independent and entrepreneurial real estate investment advisor for funds and mandates with assets under management of approximately EUR 10 billion. As a subsidiary of the Stockholm-based Catella AB, CIM advises more than 25 mutual real estate funds and special real estate funds as well as several mandates across 15 European countries, with a focus on residential, mixed-use, parking, and logistics properties. CIM provides (advisory) services in research, portfolio management, acquisitions, disposals, and asset management. The company operates offices in Berlin, Munich, and Vienna.

|

For further information: Catella Investment Management GmbH Stine Zöchling Head of Marketing and PR Office: +49 (0)30 887 285 29 76 Mobile: +49 (0)151 544 51 005

|

|

|

|

Further information can also be found on the website at www.catella.com/immobilienfonds

|

||