2025-11-27 7:29 CET, Europe, Germany | Investment Management | Press release

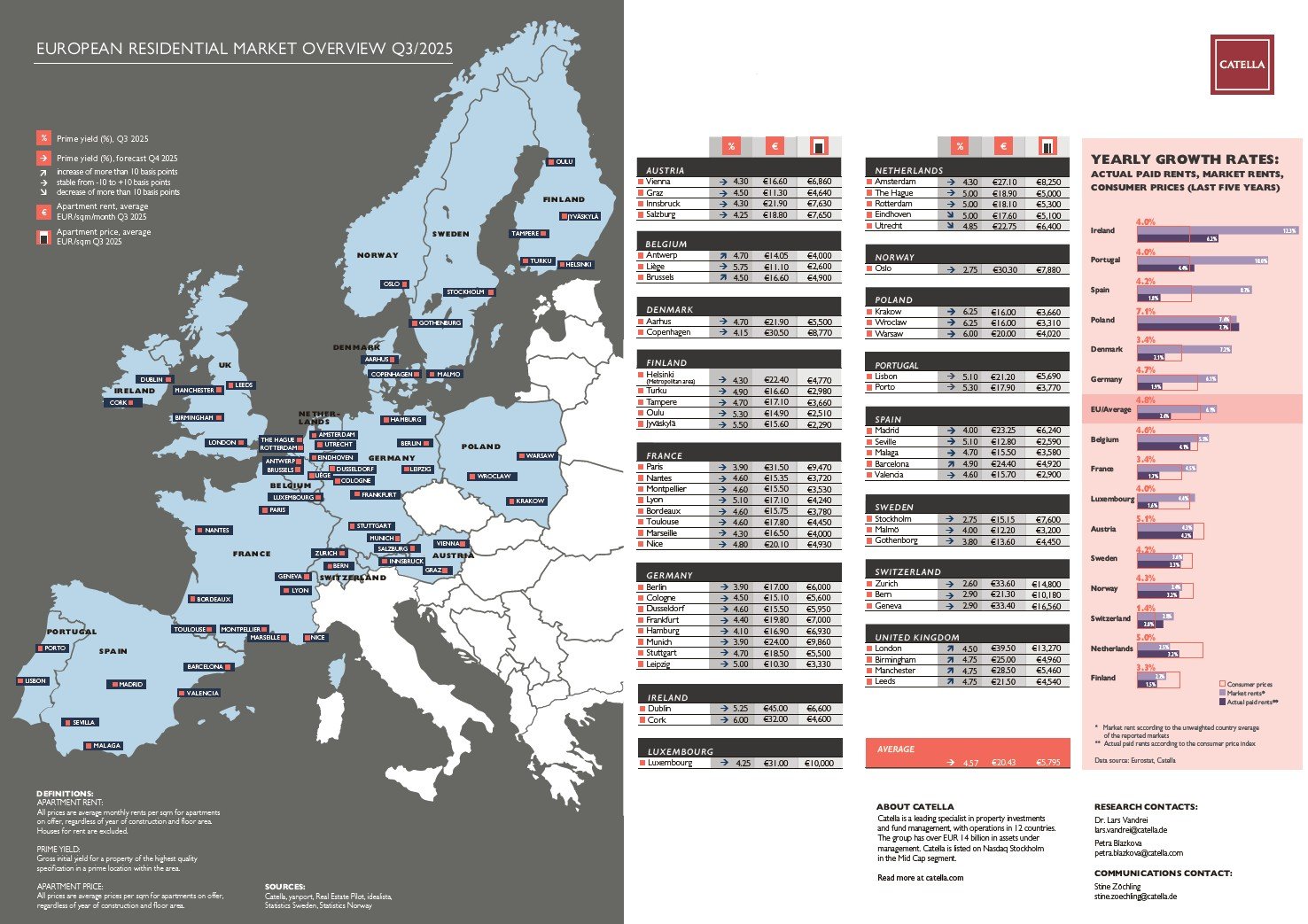

In the third quarter of 2025, the European housing market shows a steadily widening gap between rents for new leases and those in existing contracts. While rents in ongoing tenancies have risen far more slowly than other consumer prices in recent years, rents for new leases have continued to grow at an above-average pace, though momentum has eased recently. Purchase prices also continue to increase on average, while yields are stabilising. The current Catella Residential Market Overview Q3/2025, covering 59 cities across 16 European countries, provides robust supporting data.

The European Commission has identified housing shortages as a systemic challenge: according to the Commission, the EU lacks around several million affordable housing units, particularly for young and low-income households. It stresses that rental increases mainly originate from new leases and the structurally insufficient supply, rather than from existing rental contracts.

“Housing scarcity is no longer a temporary issue but a structural market distortion,” says Dr. Lars Vandrei, Head of Research at Catella Investment Management GmbH (CIM). “The widening gap between existing and new rental contracts shows that housing cost pressure arises primarily when households move – not within ongoing tenancies. The resulting market distortion lead to misallocations that are not only suboptimal for households themselves but also produce inefficient market outcomes and thus economic damage.”

Market Data: Rent Price Growth Drives Purchase Prices

Differences across markets remain substantial: while some European capitals continue to show strong rental momentum, others are clearly below average. Across all analysed markets, the unweighted average rent in Q3 2025 stand at €20.43/sqm per month, an increase of 2.1 % compared to Q1 (€20.02/sqm), and 4.5 % year-on year. Pressure remains particularly high in Ireland: Dublin again stands out with €45.00/sqm, distancing itself from Europe’s other top markets – London at €39.50/sqm and Zurich at €33.60/sqm. More affordable markets such as Leipzig (€10.30/sqm) or Liège (€11.10/sqm) remain well below the average.

Purchase prices across Europe continued to stabilise in Q3 2025: the unweighted average stands at €5,795/sqm, reflecting a moderate increase of 1.7 % over the past six months and 2.7 % year-on-year. While prime yields average at 4.57 % and therefore roughly unchanged, increases in transaction prices can be attributed to increased rents.

Focus on Germany

Across Germany’s eight largest cities, average rents across all apartment types show only marginal changes. While overall rental levels remain broadly stable, the largest cities Berlin (€17.00/sqm), Hamburg (€16.90/sqm), Munich (€24.00/sqm) and Cologne (€15.10/sqm) recorded slightly lower rents. This is primarily due to a lower share of new-build units in the dataset, which results in a larger share of (cheaper) existing units in the average.

While purchase prices for condominiums in Munich and Stuttgart have statistically decreased slightly, other German markets show rising prices compared to Q1 2025 – in particular Cologne (+5 %) and Düsseldorf (+7 %). Yields have declined in all eight major German cities: Berlin and Munich show the lowest yields at 3.90 %, while Leipzig continues to offer the highest yields at 5.00 %.

Special Topic: Mobility is restricted as “lock-in effect” intensifying

As a special topic, Catella analyses the development of market rents, actual rents paid, and consumer prices.[1] The analysis shows that, on average, housing cost burdens have not risen more strongly than other living costs. Over the past five years, consumer prices in the EU have grown by 4.8 % annually, while actual rents have increased by only 2.6 %. Only Ireland, Portugal, and Poland have seen faster growth in actual rents. Alongside Spain, with an average annual increase in market rents of 8.7 %, these are the countries where market rents have risen particularly sharply. The Netherlands is the only market besides Poland where market rents (2.5 % annually) have grown more slowly than actual rents.[2]

“Across Europe, residential rents increased the fastest in Ireland with 12.3 % annual increase over the past five years” says Petra Blazkova, Head of Catella Group Research and Strategy. “The Irish economy and its residential market, despite being more cyclical, benefitted post-Brexit and gave the country a corporate advantage in current global geopolitical uncertainties. The core problem, however, lies elsewhere: market rents based on new lease have increased twice as fast as compared to existing contracts not only in Ireland but across most European cities.”

This amplifies the so-called “lock-in effect”: households move less frequently because they cannot or do not want to afford the significantly higher rents associated with moving, even when another dwelling or location would better suit their needs. For example, labour mobility suffers when moving from Berlin to Hamburg for a job becomes unaffordable. Mobility within regional markets is also restricted: households may remain in units that have become too small, leading to increasing misallocation and overcrowding.

About Catella Investment Management GmbH (CIM)

Catella Investment Management GmbH (CIM) is an independent and entrepreneurial real estate investment advisor for funds and mandates with assets under management of approximately EUR 10 billion. As a subsidiary of the Stockholm-based Catella AB, CIM advises more than 25 mutual real estate funds and special real estate funds as well as several mandates across 15 European countries, with a focus on residential, mixed-use, parking, and logistics properties. CIM provides (advisory) services in research, portfolio management, acquisitions, disposals, and asset management. The company operates offices in Berlin, Munich, and Vienna.

|

For further information: Catella Investment Management GmbH Stine Zöchling Head of Marketing and PR Office: +49 (0)30 887 285 29 76 Mobile: +49 (0)151 544 51 005

|

|