2026-02-26 7:44 CET, Europe, Germany | Investment Management | Press release

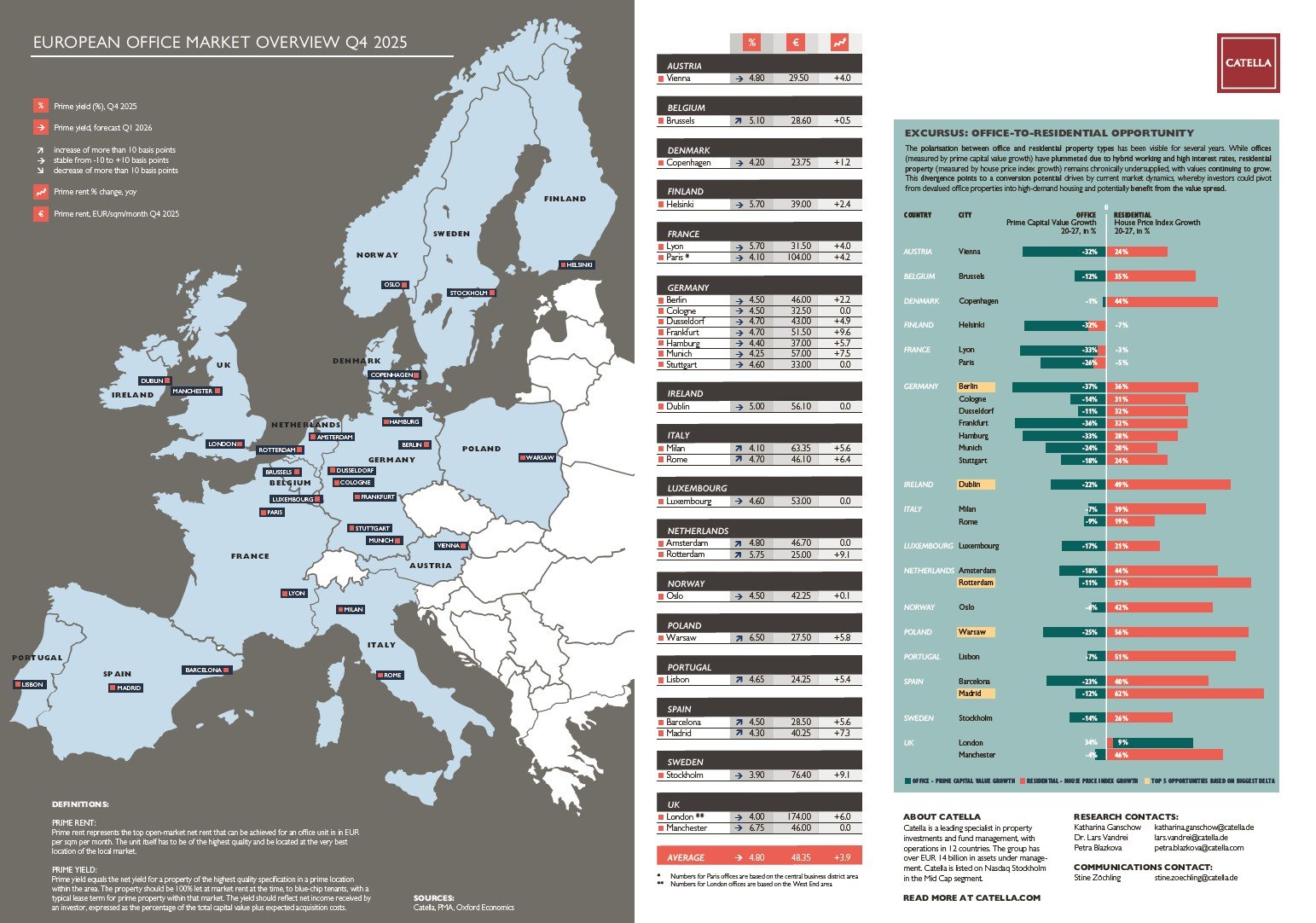

Catella has published its Office Market Overview Q4/2025, covering 27 cities across 16 European countries. Prime office rents in Europe continued to rise moderately in the fourth quarter of 2025, while prime yields remained largely stable compared with the strong adjustments seen in previous quarters. This points to an ongoing market stabilisation for high quality, CBD located office assets following the repricing phase of recent years.

Average prime rents reached EUR 48.35 per sqm per month, corresponding to average annual growth of around +3.9%, indicating continued rental growth in the prime segment, led by ongoing “flight to quality” assets in central locations. London (West End) remained the most expensive market at EUR 174.00 per sqm. Strong year-on-year rental growth was recorded in Frankfurt (+9.6%), Rotterdam (+9.1%), and Stockholm (+9.1%), while markets such as Dublin and Luxembourg recorded flat rents. Overall, none of the cities experienced a decline in prime rents.

Prime yields averaged 4.80%, remaining elevated not only due to interest rates but also because of structural shifts including higher vacancies, reduced post-pandemic income, and hybrid working. This reduced occupier demand has weakened investor appetite, though quarter-on-quarter yields remained broadly stable with only minor movements, suggesting that the valuation adjustment process in many central markets is largely complete

“If rental growth in the prime segment continues, this is likely to translate into moderate upward pressure on capital values for top-quality office properties, provided financing conditions continue to stabilize.” says Katharina Ganschow, Research Manager at Catella Investment Management GmbH (CIM).

Office-to-residential conversions

The increasing polarisation between office and residential markets is shaping investment strategies across many European cities. While prime office capital values have fallen across many markets since 2020, London (West End) stands out as an exception, recording capital value growth of +34% over the period. Comparable capital value growth rates in other markets are observed only in the residential sector, where values continue to rise significantly due to structural supply shortages. The analysis reveals pronounced differences between prime office assets and average residential prices that would be even more evident if equivalent quality segments were compared, highlighting the potential for office-to-residential conversions.

Against this backdrop, cities such as Madrid, Berlin, Dublin, Warsaw, and Rotterdam show particularly strong market potential for office-to-residential conversions. However, this potential cannot be transferred across all assets indiscriminately. In addition to economic factors, building characteristics, technical standards and planning and zoning regulations play a decisive role in determining feasibility. Assets that were originally designed with a degree of use flexibility stand to benefit in particular. Execution risk is higher than in other strategies, making careful asset selection and clear CapEx requirements critical.

About Catella Investment Management GmbH (CIM)

Catella Investment Management GmbH (CIM) is an independent and entrepreneurial real estate investment advisor for funds and mandates with assets under management of approximately EUR 10 billion. As a subsidiary of the Stockholm-based Catella AB, CIM advises more than 25 mutual real estate funds and special real estate funds as well as several mandates across 15 European countries, with a focus on residential, mixed-use, parking, and logistics properties. CIM provides (advisory) services in research, portfolio management, acquisitions, disposals, and asset management. The company operates offices in Berlin, Munich, and Vienna.

|

For further information: Catella Investment Management GmbH Stine Zöchling Head of Marketing and Public Relations Office: +49 (0)30 887 285 29 76 Mobile: +49 (0)151 544 51 005 |