2026-05-27 8:05 CET, Europe, Germany | Investment Management | Press release

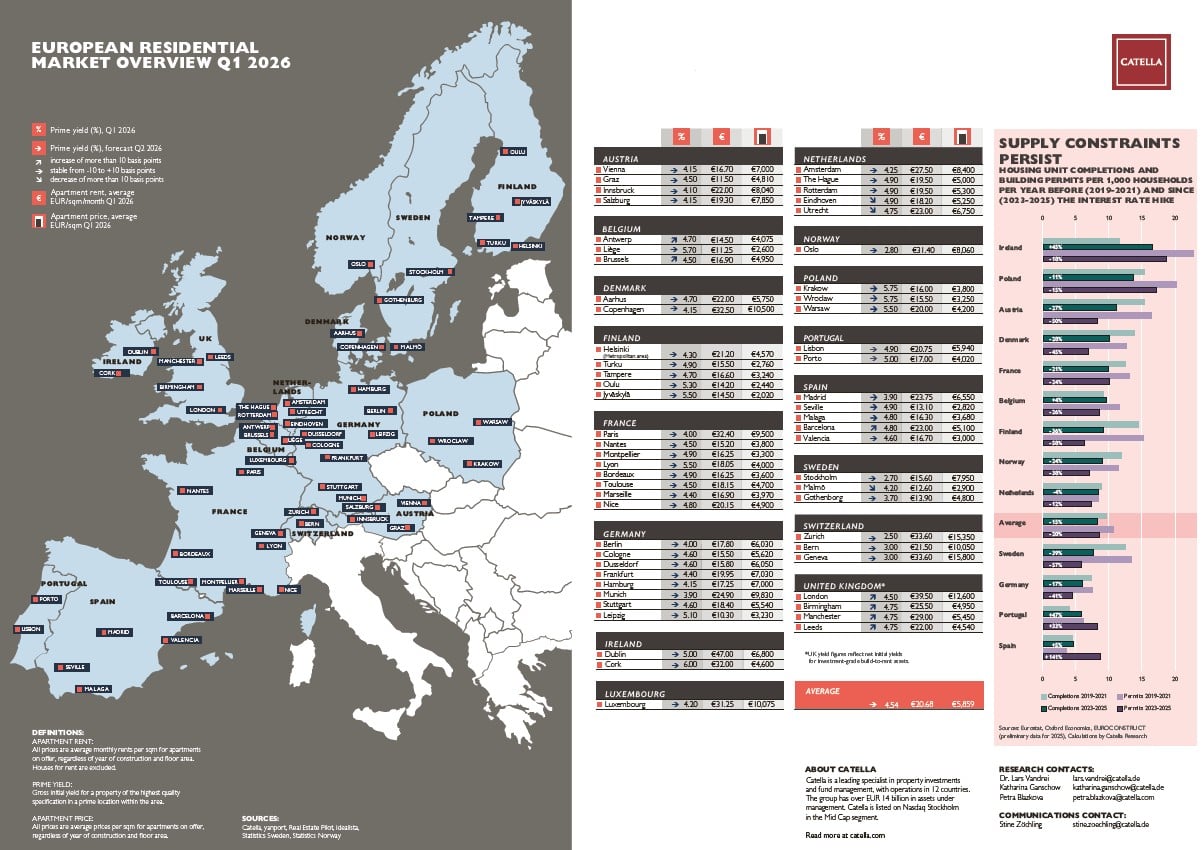

Catella Residential Market Overview for Q1 2026 shows that supply shortages across European housing markets are expected to further deepen. Recent trends in residential completions and building permits clearly point to a continued imbalance between housing demand and supply across the region. The semi-annual report provides reliable data based on 59 cities in 16 European countries.

- The sharpest declines are concentrated in Northern Europe (Finland, Sweden and Denmark), where permits have halved since 2022.

- Southern Europe diverges but from a structurally low base – Spain records the lowest level of new homes per household in the peer group.

- Price dynamics remain resilient based on European averages, with rents and sales values increasing by 3.3% and 2.9% respectively.

According to the report, housing completions across the analysed countries dropped by approximately 15% on average in the 2023-25 period compared to 2019-21. Looking ahead to a future supply, new building permits — a leading indicator of completions — declined even more steeply, by around 20% over the same period, pointing to further contractions in housing delivery ahead.

“The data shows that the European housing shortage remains primarily a supply challenge,” says Dr. Lars Vandrei, Head of Research at Catella Investment Management GmbH (CIM). “For many European cities any relief to tight housing markets is being further delayed with the structural, excess demand unlikely being met in the coming years.”

Declining permits weigh on future new construction pipeline

The declines in several Northern and Central European markets are particularly striking. In Finland, completions declined by 36% and permits by 58%, while Sweden recorded falls of 39% and 57%, respectively. Austria and Denmark also experienced marked slowdowns across key supply indicators.

By contrast, Southern Europe shows a different dynamic. Spain and Portugal are the only markets to report increases in both permits and completions. The new supply, however, remains insufficient to materially ease demand pressure in core markets such as Madrid, Barcelona and Lisbon.

Ireland also stands out with the highest level of construction activity per 1,000 households. The imbalance between supply and demand, however, persists. Underpinned by strong economic and population growth, Dublin remains the most expensive rental market in Europe, with new lease rents averaging €47.00/sqm.

Across all analysed cities, the average new lease rent reached €20.68/sqm in Q1 2026, marking a moderate increase compared to six months earlier (€20.43). Markets driven by strong international demand continue to command the highest rents – Dublin is followed by London, Zurich and Geneva.

Housing regulations impact market pricing with local dynamics varying significantly

European prime yields remain broadly stable at 4.54%, compared with 4.57% six months ago, although policy changes are influencing local dynamics. In the Netherlands, recently implemented lower transfer taxes have supported pricing and driven yield compression. By contrast, higher transaction taxes in Barcelona are likely to create upward pressure on yields over time, even if stable for now at 4.80%.

At the same time, average condominium prices across Europe increased marginally to €5,859/sqm (Q3 2025: €5,795/sqm), driven by high‑income, supply‑constrained markets with strong international demand. Swiss cities – Geneva and Zurich – lead, followed by London, Luxembourg and Bern.

“Housing regulations have been a key driver of pricing and potential yield movement across European markets,” says Petra Blazkova, Head of Catella Group Research and Strategy. “Changes in transaction taxes, as seen in the Netherlands and Barcelona, directly impact investment behaviour and pricing, reinforcing the importance of local market dynamics alongside structural demand in high-income, supply-constrained cities.”

Deep Dive Germany: Munich remains the most expensive market

Germany is substantially affected by the deepening limitations of housing supply. The number of completions per 1,000 households declined by 17% between 2023 and 2025 compared to the same period between 2019 and 2021. Permits dropped by 41% over the same timeframe. It is clear that this supply dynamic is driving the average rental growth – the rents have increased aligned with inflation since Q3 2025. In Berlin and Munich, the average rental growth was the highest: 5% and 4% respectively over the same period. The most expensive rental city in Germany – Munich – average rent currently stands at €24.90. The city also records the highest residential purchase prices, at €9,830/sqm in Q1 2026, followed by Frankfurt and Hamburg.

Looking forward, the German residential market is likely to remain multi-faceted from an investor’s perspective. Prime yields in Germany range between 3.90% in Munich and 5.10% in Leipzig. While major metropolitan areas are characterized by both high purchase price and rental levels, more peripheral markets such as Leipzig continue to offer comparatively high yields at significantly lower entry prices.

Download the map here

About Catella Investment Management GmbH (CIM)

Catella Investment Management GmbH (CIM) is an independent and entrepreneurial real estate investment advisor for funds and mandates with assets under management of approximately EUR 10 billion. As a subsidiary of the Stockholm-based Catella AB, CIM advises more than 25 mutual real estate funds and special real estate funds as well as several mandates across 15 European countries, with a focus on residential, mixed-use, parking, and logistics properties. CIM provides (advisory) services in research, portfolio management, acquisitions, disposals, and asset management. The company operates offices in Berlin, Munich, and Vienna.

For further information:

Catella Investment Management GmbH

Stine Zöchling

Head of Marketing and Public Relations

Office: +49 (0)30 887 285 29 76

Mobile: +49 (0)151 544 51 005

Email: stine.zoechling@catella.de

Disclaimer:

This is a marketing release. It is for information purposes only and does not constitute investment advice, an investment recommendation, an offer or an invitation to buy or sell investment products. The information is not suitable for making a concrete investment decision on its basis. It does not contain any legal or tax advice. The provision of the information does not create any contractual obligation or any other liability towards the recipient or third parties. Shares may only be purchased on the basis of the currently valid Terms and Conditions of Investment in conjunction with the currently valid Sales Prospectus.